Corporate

5 things Malaysian employers pay on top of your monthly salary

about 7 years ago JS LimHave you ever wondered what it would be like to open your own business? This comes with the freedom to do what you want, the way you want to, but it obviously comes with having to take on the responsibilities that an employer handles. There are lots of challenges that you might not be sure how to tackle because well, no one teaches you these things in school.

The biggest challenge people usually think of is capital (although this case study tells us otherwise). You need to pay rent, overhead costs, employees’ salaries… But if you’ve never been an employer, you might not have known that salaries are not all that a boss pays to hire people. There’s definitely the smaller expenses like paying a lawyer to draft the employment contract and getting a team to manage payroll, but there are also recurring expenses that come from hiring employees.

You most likely already know about at least 2 of them (probably EPF and SOCSO,right?), but might not have known some of the details behind how they work. With that, here are 5 recurring payments your boss is probably making on top of your monthly salary.

1. SOCSO - Social Security Organization

Also known as PERKESO in Malay (Pertubuhan Keselamatan Sosial Malaysia), SOCSO is a government agency set up under the Employees’ Social Security Act 1969 that runs a social security fund for Malaysians.

There are two main schemes managed by SOCSO. The first is the Employment Injury Scheme, which is basically an insurance fund for all Malaysians if and when workplace accidents occur. It also covers occupational diseases, like loss of hearing from loud noises at the workplace. The second scheme is the Invalidity Scheme, which provides benefits for employees who suffer from total or permanent disability, making them no longer capable of earning a living. Unlike the Employment Injury Scheme, this covers incidents that aren’t related to your job as well.

Unless you fall under one of the rare exceptions, you’ll see your SOCSO contribution as a deduction on your payslips each month, and the law requires your employer to contribute as well. The contributions are based upon a fixed table based on how much you earn, which increases with your salary up till you’re earning RM4,000.

For example, if you earn between RM2,400 and RM2,500, you have to contribute RM12.25 every month. But your employer has to contribute much more (about 1.75%) at RM42.85, plus an extra RM30.60 towards the Employment Injury Scheme in particular. If you’re doing a risky job for a company, it makes sense for them to take some responsibility if you get injured.

You can find a complete table of the contribution amounts at SOCSO’s website.

2. EPF - Employees Provident Fund (duh!)

The most obvious of the contributions, but it’s worth mentioning. You probably already know about EPF even if you don’t know the details about how it works. It’s a fund you contribute to that makes investments to grow your money, which will sustain you after you retire.

Looking at your payslip, you’ll see that you contribute 11% of your salary every month, which gets deducted from your gross pay (bye bye 11% straight away). We’ve all probably wished that we could keep the 11% from time to time, but hey, at least it’s tax deductible. If you’re not that familiar with our tax reliefs, you’ll want to know that you can get relief on up to RM6,000 per year for contributions to your EPF and life insurance. And there’s another RM3,000 in relief if you contribute to a registered Private Retirement Scheme (PRS).

[READ MORE - 5 sources of income that are tax free in Malaysia]

What you might not keep in mind is that your boss also has to contribute to your EPF account by law. Depending on how much you earn, your employer pays an extra 13% of your gross salary to your EPF, making your “real” salary actually 13% higher than what you see. If you earn more than RM5,000 per month, then your employer pays 12% instead.

You might never see that money until you turn 55, but it’s still yours later on. Not to mention, it’s a real expense for your boss that they have to pay right away - which might be something to keep in mind to help you negotiate your salary in future.

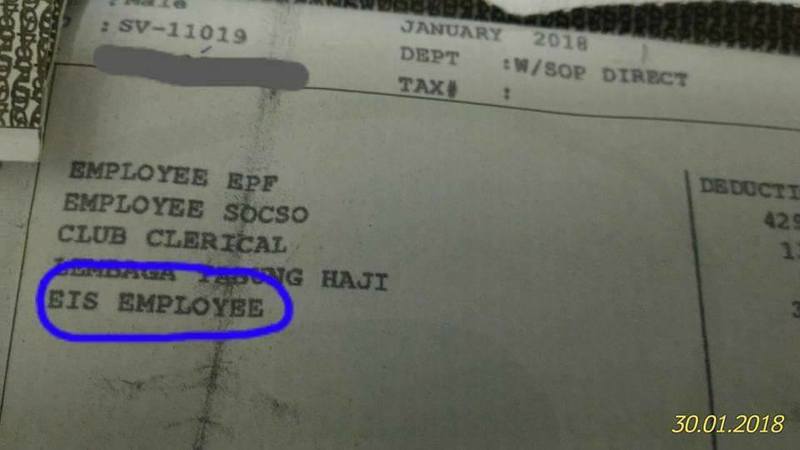

3. EIS - Employment Insurance System

If you didn’t hear about it when the law came into effect, you might have been one of the people wondering “why my pay suddenly kena cut?” in January 2018. Your pay technically didn’t get cut, but you were obligated to contribute to this relatively new scheme. We covered how it works in our earlier article:

[READ MORE - Malaysia's new insurance system automatically deducts your salary but...for what?]

Basically, it’s a scheme that covers people who have lost their jobs through no fault of their own (we cover the exact list in our article above as well).

This includes situations where your boss fires you for no good reason, if colleagues make life really difficult for you, and even when you are threatened or sexually harassed.

[READ MORE - My boss just fired me for no reason, what can I do now?]

Both you and your employer have to pay 0.2% of your salary each for the EIS. The two main benefits employees get out of the EIS are:

i) Career counselling and job training

This is poised to help the newly unemployed find new work, and even transition into a new industry if they have to.

ii) Unemployment payouts

Employees in Malaysia will be getting a portion of their salary for up to 6 months after losing their job. It’s meant to help stabilize people’s finances while they look for work, so the time limitation prevents abuse by people who would rather not look for a job. The exact rates are in the Third Schedule of the Employment Insurance System Act 2017.

If you ever need to make an EIS claim, you can make it through SOCSO’s dedicated website for the EIS over here.

4. HRDF - Human Resource Development Fund

Certain companies in manufacturing, service, and mining need to pay another levy under the Pembangunan Sumber Manusia Berhad Act 2001, which manages the Human Resource Development Fund (HRDF) of Malaysia. They facilitate training programs to upgrade worker skills in Malaysia.

The law behind their formation basically requires companies to commit some money to training their employees, by paying 1% of their employees’ salaries to the fund, which they can use in the form of training grants to send their employees to training programs that benefit their industry.

For example, a hotel company who has paid money to the HRDF can send their employees to a workshop where they learn about improving the hotel’s operations. But a computer chip factory might get their workers to learn about avoiding workplace accidents. The training programs must come from training providers registered with the HRDF.

If you work in one of the above industries, chances are your employer is a registered company under the HRDF, and you might want to ask about training programs if you haven’t been sent for any. The exact criteria are quite specific so you may have to check if your company qualifies in the first place (usually very small companies are not required to take part). There’s a complete (and LONG) list of companies specified in the First Schedule of the Pembangunan Sumber Manusia Berhad Act.

5. Professional Insurance

In any profession, accidents and mistakes happen from time to time - whether it’s a valet who accidentally crashes a customer’s car, or as simple as people falling from a wet floor. But who’s responsible for them? Your boss.

[READ MORE - Your boss is responsible because of a legal principle called “vicarious liability”]

Even if you’re the most careful and detail-oriented person in the world, accidents are sometimes simply unavoidable. Freak accidents can happen and we may never anticipate them perfectly - but it helps to be prepared. This is why companies in certain industries like medicine, law, advertising, and architecture may purchase what is called professional indemnity insurance to cover any unforeseen losses that might occur - just in case.

As an example, back in 2009 the $35 million rebranding of Tropicana (the popular orange juice from PepsiCo) actually caused a 20% drop in sales instead of having a positive effect on the brand. We don’t actually know what happened behind the scenes for this incident, but sometimes, the company responsible has to foot the costs. And if some employees were found to be at fault, they can actually be held responsible for the losses personally.

The cost of professional insurance varies from industry to industry, and is usually determined by the insurance company.

There’s more behind what’s written on your payslip

Those were just 5 things employers need to foot for their employees in Malaysia. If you’ve ever heard of any other types, do let us know!

It’s doesn’t always feel good for companies and employees to have to make all these extra payments, but it’s a way to create some form of assurance that you’ll be taken care of throughout and after your career. A few hundred Ringgit a month does feel like a lot, but it definitely beats facing a big problem later on with not enough resources to help ourselves.

Jie Sheng knows a little bit about a lot, and a lot about a little bit. He swings between making bad puns and looking overly serious at screens. People call him "ginseng" because he's healthy and bitter, not because they can't say his name properly.