Consumer,Banking,Sponsored

If your bank closes down in Malaysia, what happens to your money?

almost 6 years ago Sponsored ContentThe concept of money has evolved throughout the past 40,000 years, from pretty shells and precious minerals in the Bronze Age to the digital numbers that you see in your banking app when payday arrives. But keeping very closely behind the evolution of money is another form of evolution – how to keep your money safe.

It really wasn’t that long ago when the highest form of security for your cash was to literally sleep on it or hide it in a freezer (cold hard cash, amirite?), and this eventually moved to the idea of keeping it in banks or investments. But the thing is, this isn’t 100% safe either as investments can be lost and banks can also become bankrupt if the economy tanks or when customers panic and withdraw their deposits en-masse (called a bank run).

So just like how you’d get an insurance policy in case something bad happens to you, this is where the concept of an ‘insurance policy’ for your bank account comes in. If you have a bank account, listen to the radio, or read some of our previous articles; there’s a pretty high chance you would have come across PIDM or Perbadanan Insurans Deposit Malaysia.

From reading the comments on our previous articles, we sort of got the idea that while most people know what PIDM is, they aren’t exactly sure of how the coverage actually works. So we thought it would be interesting to compile these comments and get an answer for them… straight from PIDM.

The easy part: What does PIDM actually do?

In case you haven’t been paying attention to the ads, here’s a quick introduction to get you up to speed.

PIDM is an agency formed under the Malaysia Deposit Insurance Corporation Act 2011 (MDIC Act 2011) to promote the stability of the financial system in Malaysia by insuring your bank deposits and insurance policies/Takaful certificates in the event a PIDM member bank or insurer goes bankrupt. These two forms of coverage are known as:

- DIS (Deposit Insurance System) – Coverage for your bank deposits, if your bank is unable to return that money to you. Protection is limited to RM250,000 per depositor, per member bank.

- TIPS (Takaful and Insurance Benefits Protection System) – Coverage for your Takaful certificates and insurance benefits, if the Takaful operator or insurance company is unable to honor the benefits covered under your insurance policy or Takaful certificate. Protection is up to RM500,000 or more depending on the type of benefits, so click here for the full list of benefits protected by PIDM.

Oh, and this coverage is free and automatically provided by PIDM!

So, that’s the easy part. For the more advanced stuff, we’ll be focusing on the bank deposit (DIS) questions to keep things less confusing. Let’s start with the most common question we see in the comments….

1. My bank told me they’re not insured…?

As of today, PIDM covers 92 member institutions – 42 member banks and 50 insurer members – meaning that most, but not all, banks are members. Member banks are all commercial and Islamic banks defined under Section 36 of the Malaysia Deposit Insurance Corporation Act 2011 as follows:

… and are automatically required to be members of PIDM, regardless of whether it’s a local bank or a foreign bank operating in Malaysia.

PIDM provides a list of member banks here, so to answer the question in the screenshot above; Bank Muamalat is a PIDM member while Bank Rakyat is not because – FUN FACT – Bank Rakyat is a development financial institution regulated under a different Act called the Development Financial Institutions Act 2002.

If you want to know whether your bank is a member ban of PIDM, the easiest way is to refer to the member bank list linked above, or you can look out for the PIDM sticker placed at the entrance of their branches. Pro tip – you can also ask your bank!

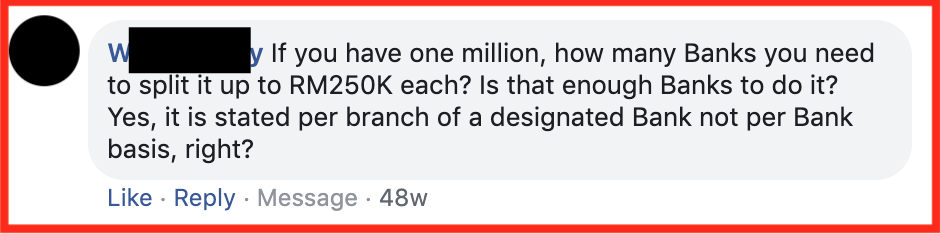

2. I have RM300k. Does this mean I need to open TWO bank accounts?

To the person with RM100 billion in their account – can we be your friend?

We’re assuming that the question is a hypothetical one but, jokes aside, yes – you can split your money across different accounts and/or banks to maximize your coverage. PIDM explains that there are three ways to do this…

“PIDM's protection is applied separately per depositor per member bank. If you have RM250,000 with Bank A and RM250,000 with Bank B, the amount protected is RM500,000 if both Bank A and B become bankrupt.” – PIDM

Yup, if you have RM1 million, you could open deposit accounts in four banks to fully protect the amount. However, do take note that this applies to separate banks and not bank branches. Currently, 42 commercial and Islamic banks are member banks of PIDM (full list here)

“To receive separate protection, you can open different types of deposit accounts within one bank. For example, apart from an individual savings account, you can also open joint-name accounts, [and others]”

If you aren’t too keen on the idea of having 4 different banking apps on your phone to manage your massive moolah, you can actually open different types of accounts within the same bank.

For example, your million Ringgit can be split into:

- an individual account (in your own name),

- a joint account with your spouse,

- a trust account for your son, and

- a trust account for your daughter

… within the same bank to be fully protected. Click here to check out the different categories of deposit accounts.

“You can also opt to open both a conventional and an Islamic account with your bank to enjoy separate protection from PIDM.”

Just to clarify, if you have RM250k in a regular savings account and RM250k in a Islamic savings account within the same bank, you’re also covered for a total of RM500k.

Click this link for examples of how the coverage will work.

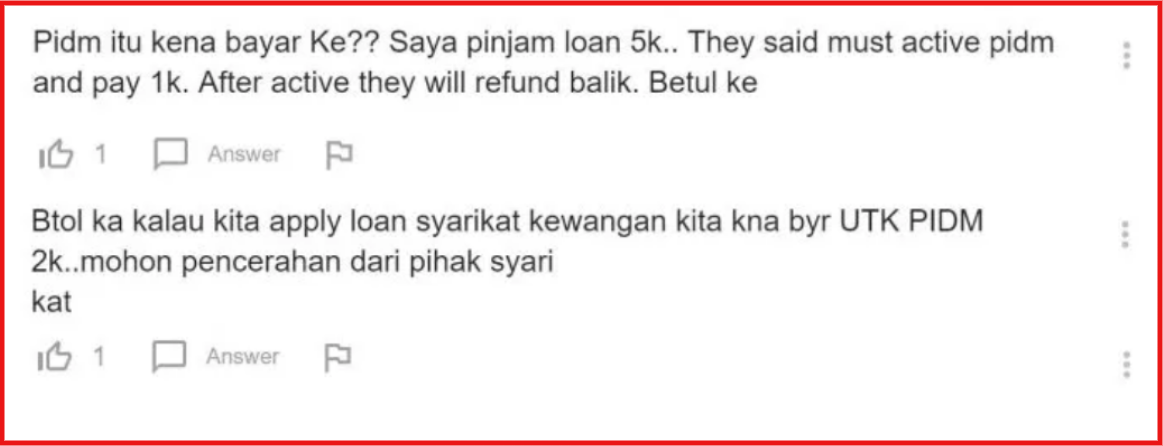

3. Will I be charged by PIDM every time I deposit money or take a loan?

So, PIDM reiterated to us that their mandate is to protect deposits, not loans. It’s a frequent point of confusion because accepting deposits and providing loans are a bank’s main business.

“Let’s take a moment to think about the mechanics of a loan – if a bank goes bankrupt, the bank does not “owe” you any money so there’s no such thing as “protection” here.

But if you have a bank deposit account, you would want to be assured that you can get back your money if the bank goes bankrupt, so this is where PIDM comes in.” – PIDM

While comparing PIDM protection to insurance is a good way to get the understanding across, it’s not entirely the most accurate. This is because, while you need to sign up for a policy and pay premiums to an insurance company for protection, PIDM’s coverage is free and automatic.

“The protection is automatic and free – no sign-ups or fees required. We will also not ask for your personal and/or financial details.” – PIDM

In other words, if you ever receive a call or message asking you to verify your personal details or pay a fee to PIDM, you can confidently tell the caller where to deposit their lies (hint: it’s a place where the sun don’t shine) because it’s definitely a scam. Similarly, if someone tells you that you need to make a payment to PIDM to protect your bank deposits, loan, or investment; that’s a scam as well.

[READ MORE: Asked to pay for PIDM protection? That’s a scam!]

The money that PIDM will use to pay you actually comes from the member institutions themselves. Basically member banks and insurer members pay annual premiums/levies to PIDM, which then goes into funds that will be used to make payments to you when needed. On that note...

4. Will PIDM protect my Amanah Saham, or against robberies/cyberattacks?

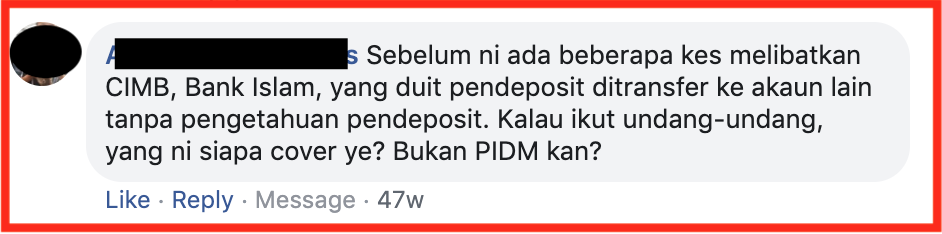

The quick answer to this is no, as PIDM only protects your money if a member bank goes bankrupt. So it’s mainly for deposits saved with its member banks and does not cover investments.

In cases of fraud, scams, natural disasters, fire, robbery, or a cyber-attack on your bank, the payment will come from the bank itself, and is dealt with on a case-by-case basis.

As a reference though, here’s a list of products that fall under PIDM’s protection (again, under the conditions that a bank goes bankrupt and within the RM250k per depositor limit)

- Savings accounts

- Current accounts

- Fixed deposits

- Islamic deposit accounts (e.g. wadiah deposit)

- Bank drafts, cheques, and any other payment instructions/instruments made against a deposit account

You will enjoy PIDM’s protection for these products whether they’re denominated in Ringgit or foreign currencies.

And, here’s what’s NOT protected:

- Deposits not payable in Malaysia

- Interbank money market placements

- Negotiable instruments of deposit and other bearer deposits

- Repurchase agreements

- Unit trusts (such as Amanah Saham), stocks, and shares

- Gold-related investment products/accounts and Islamic Investment accounts

To be on the safer side, you can always check with your bank to see if PIDM protects your deposit. According to PIDM, a member bank must inform you whether or not your deposit is eligible for the deposit insurance protection before you place your money with them. Member banks would also have a list of deposit products that are eligible for deposit insurance protection displayed in their premises or websites.

5. Wait… how will PIDM return my money? Cheque ah?

This question was actually asked by one of our interns after we published our first article on PIDM, and we… had no idea.

As it turns out, there is little action that needs to be taken from the customer’s side – you don’t need to apply, make a report, or open a new bank account somewhere else.

“You do not need to make a claim. PIDM will announce how and when reimbursement of insured deposits will be made. PIDM will base its reimbursement on the depositor records obtained from the member bank.

It is important to keep your record updated at your bank”

PIDM will make payments on insured deposits to customers if a winding up (going out of business) order has been made in respect of a member bank. They will reimburse the insured deposits as soon as possible, and no longer than three months from the date of the winding up order.

In such a scenario, PIDM will make public announcements to notify depositors on how and when the payment of insured deposits will be made. They will also make communications channels – including its call centres and website – available for you to find out the status of you insured deposits.

Bonus: Why does PIDM even need to advertise themselves?

This question popped up way too often for us to leave out, and the response is:

“Firefighters are called to protect the public in emergency situations. These days, firefighters have expanded their role to be more involved with the community. They raise awareness, conduct fire safety checks and communicate fire prevention and other safety messages to the public.

PIDM’s role is very much similar to that of the firefighters’ but within the context of the financial system.”

Other than the protection it offers, PIDM is pretty big on educating the public in financial literacy. Their Facebook Page is a channel for you to ask your burning questions on PIDM protection.

They’re always open to more questions, so let us know if you have any more (don’t forget, they cover Takaful and insurance benefits as well) and we might do a part 2. Otherwise, you can always call their toll-free line at 1-800-88-1266 or visit their website linked here.